AWM Performance Monitor – July 2020

Note From The Managing Director.

The month saw a rebalance to the CBAM portfolio positions and the maintenance of a gold overweight in those portfolios has, in particular, helped spur the positive July returns vs other parts of the world. In addition after pain on the way down the Active US equity fund that the portfolios hold has both protected from the close to 6% rally in the £ vs the $ after being a missed opportunity cost in March.

We see this continuing so expect no change in this fund and its positioning for the rest of 2020. We get great data as an investment team in running our lean and efficient passive driven funds but still maintaining active managers in many parts of the world.

The last 3 months has really been one where active managers have earned their fees and we will keep an open mind as to whether we bring this back to the closer 50/50 historic split. This will increase portfolio cost but if you look at July all 5 top performers were actively management positions.

Year to date we are really happy to have portfolios back to where they are given the market challenges we have faced.

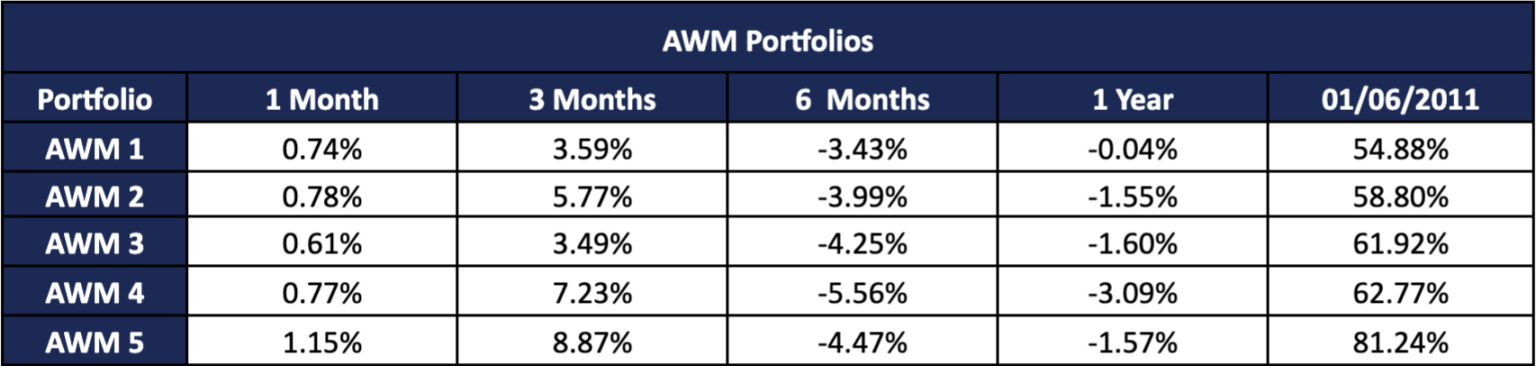

AWM Portfolio Performance

These tables simply indicate AWM’s portfolio’s over the stated time periods up to 31/07/2020.

Market Update

It has been yet another encouraging month with all portfolios showing a solid performance (on average +1.29% over the month). This is rather impressive when consideration is paid to the fact that the “big three” indices of the FTSE 100 & EUROSTOXX50 & S&P500 (covering UK, Eurozone & USA) finished down 4.01%, 1.19% & 0.27% respectively. Since the portfolio low of 23rd March, the portfolio has returned between 11.22% (AWM1) & 26.49% (AWM5).

The rebalance of July 2020 has so far performed in line with expectation, which gives us confidence in the positioning of our portfolios for the remainder of Q3 2020.

Click through to the performance graphs for longer-term overviews and versus world indices.

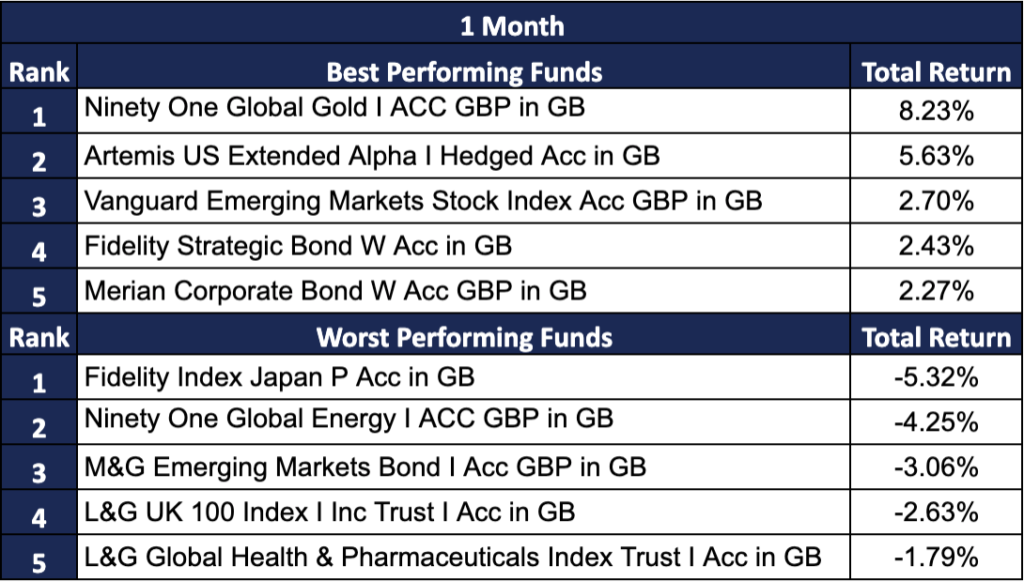

Best and Worst Performing Funds

This table simply indicates a portion of the AWM’s chosen invested funds, which are either the best performing or worst performing, over the stated time periods up to 31/07/2020.

This information is correct and up to date as of 09/07/2020.

This Performance Monitor has been created from multiple sources as well as our own views and this should not be taken as investment advice. If you require financial advice then please contact us by email or phone so that you can speak to a qualified financial adviser. Any information provided/gathered will be subject to the General Data Protection Regulation (GDPR). You may be assured that we and any company associated with Ascot Wealth Management will treat all personal data and sensitive personal data and will not process it other than for a legitimate purpose.

Ascot Wealth Management Limited is authorised and regulated by the Financial Conduct Authority reference 551744. Our registered office: Scotch Corner, London Road, Sunningdale, Ascot, Berkshire, SL5 0ER. Registered in England No. 7428363. www.old.ascotwm.com Unless otherwise stated, the information in this document was valid on 3rd February 2017. Not all the services and investments described are regulated by the Financial Conduct Authority (FCA). Tax, trust and company administration services are not authorised and regulated by the Financial Conduct Authority. The services described may not be suitable for all and you should seek appropriate advice. This document is not intended as an offer or solicitation for the purpose or sale of any financial instrument by Ascot Wealth Management Limited. The information and opinions expressed herein are considered valid at publication, but are subject to change without notice and their accuracy and completeness cannot be guaranteed. No part of this document may be reproduced in any manner without prior permission. © 2017 Ascot Wealth Management Ltd. Please note: This website uses cookies. To continue to use this website, you are giving consent to cookies being used.

")